Business, 24.05.2021 15:10 0IggyMarie0

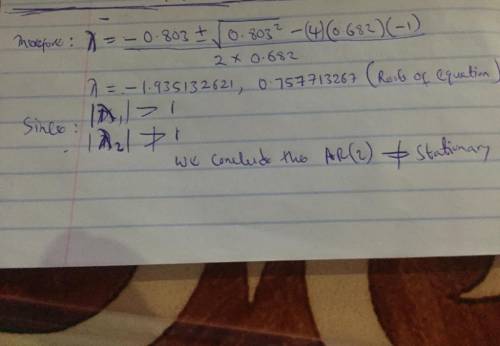

You obtain the following estimates for an AR(2) model of some returns data

yt = 0.803yt−1 + 0.682yt−2 + ut

Where ut is a white noise error process. By examining the characteristic equation, check the estimated model for stationarity.

Answers: 3

Other questions on the subject: Business

Business, 22.06.2019 11:00, ashlynmartinezoz2eys

When the federal reserve buys bonds from or sells bonds to member banks, it is called monetary policy reserve ratio interest rate adjustment open market operations

Answers: 1

Business, 23.06.2019 00:50, aaronlikly

On december 31 of the current year, the unadjusted trial balance of a company using the percent of receivables method to estimate bad debt included the following: accounts receivable, debit balance of $97,900; allowance for doubtful accounts, credit balance of $1,031. what amount should be debited to bad debts expense, assuming 6% of outstanding accounts receivable at the end of the current year are estimated to be uncollectible?

Answers: 1

Business, 23.06.2019 05:30, sabaheshmat200

What is a potential negative effect of an expansionary policy? decreased borrowing increased interest rates increased inflation decreased available credit

Answers: 1

You know the right answer?

You obtain the following estimates for an AR(2) model of some returns data

yt = 0.803yt−1 + 0.682yt...

Questions in other subjects:

Mathematics, 14.11.2019 22:31

Advanced Placement (AP), 14.11.2019 22:31

Business, 14.11.2019 22:31

Chemistry, 14.11.2019 22:31

Mathematics, 14.11.2019 22:31

Biology, 14.11.2019 22:31

Mathematics, 14.11.2019 22:31