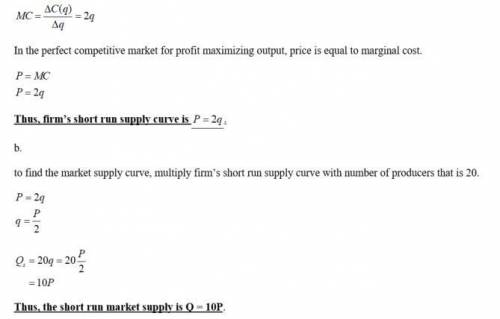

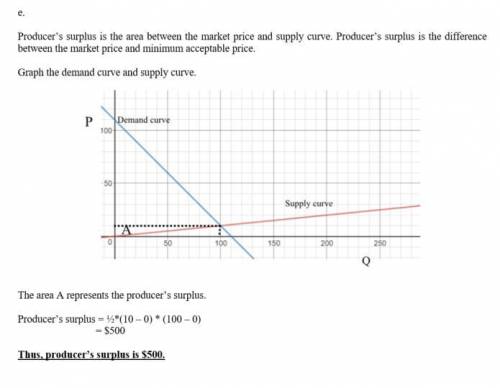

The bolt-making industry currently consists of 20 producers, all of whom operate with the identical short-run total cost curves �(�) = 16 + �), where q is the annual output of a firm. The market demand for bolts is �- = 110 − � (assume that the industry is perfectly competitive). a. What is the firm's short-run supply curve? b. What is the short-run market supply curve? c. Determine the short-run equilibrium price and quantity in this industry. d. What is each firm’s profit? e. What is the aggregate producer surplus?

Answers: 2

Other questions on the subject: Business

Business, 22.06.2019 06:00, Tayj91

Why might a business based on a fad be a good idea? question 2 options: fads bring in the most customers. some fads are longer lasting than expected. fads have made some business owners incredibly wealthy. fads can take a business in a new direction.

Answers: 2

Business, 22.06.2019 11:10, AM28

Your team has identified the risks on the project and determined their risk score. the team is in the midst of determining what strategies to put in place should the risks occur. after some discussion, the team members have determined that the risk of losing their network administrator is a risk they'll just deal with if and when it occurs. although they think it's a possibility and the impact would be significant, they've decided to simply deal with it after the fact. which of the following is true regarding this question? a. this is a positive response strategy. b. this is a negative response strategy. c. this is a response strategy for either positive or negative risk known as contingency planning. d. this is a response strategy for either positive or negative risks known as passive acceptance.

Answers: 2

Business, 22.06.2019 17:00, PlzNoToxicBan

Cadbury has a chocolate factory in dunedin, new zealand. for easter, it makes two kinds of “easter eggs”: milk chocolate and dark chocolate. it cycles between producing milk and dark chocolate eggs. the table below provides data on these two products. demand (lbs per hour) milk: 500 dark: 200 switchover time (minutes) milk: 60 dark: 30 production rate per hour milk: 800 dark: 800 for example, it takes 30 minutes to switch production from milk to dark chocolate. demand for milk chocolate is higher (500lbs per hour versus 200 lbs per hour), but the line produces them at the same rate (when operating): 800 lbs per hour. a : suppose cadbury produces 2,334lbs milk chocolate and 1,652 lbs of dark chocolate in each cycle. what would be the maximum inventory (lbs) of milk chocolate? b : how many lbs of milk and dark chocolate should be produced with each cycle so as to satisfy demand while minimizing inventory?

Answers: 2

You know the right answer?

The bolt-making industry currently consists of 20 producers, all of whom operate with the identical...

Questions in other subjects:

Mathematics, 31.03.2020 21:23

Biology, 31.03.2020 21:23

Mathematics, 31.03.2020 21:23

History, 31.03.2020 21:23